Just weeks ago, the share price for GameStop, a brick-and-mortar retailer of video games, saw its shares go from $17 to $483 before plummeting back down to around $50 within the span of a month. The story gripped the media (the subject of more than 3,000 articles) and the public’s attention, painted as a David vs. Goliath story: small, plucky retail investors (non-professional individual investors) were taking on institutional investors (billion dollar firms, such as hedge funds, that invest with pooled resources) — and supposedly winning big. The soaring stock price finally crashed when popular trading platforms like Robinhood limited stock trading, coincidentally providing a way out for institutional investors who had been betting on the stock going down.

Now, accusations are flying from both sides. Retail investors worry about collusion between Wall Street and trading platforms, whose decision to limit trading effectively put an end to the short squeeze that big funds were trapped in. Meanwhile, Wall Street has lodged complaints about market manipulation that cost them billions. So, what really happened? Does the incident stand up to its underdog narrative or is it evidence that the stock market unfairly benefits Wall Street firms over everyday Americans? This week, The Factual looked at highly rated news articles from 20 sources across the political spectrum to find some answers.

What is shorting? Shorting is when an investor bets against a stock rising in the future. During a short, an investor “borrows” shares of a specific stock and immediately sells them with the intention of buying the same number of shares back at a later date, for a lower price, before returning them to the original owner. If the stock depreciates over that period, the borrower gets to pocket the difference between the initial selling price and the later purchasing price. However, if the stock price increases, the borrower ends up losing money since they have to repurchase shares at a higher price before returning them. In January, institutional investors were shorting GME on a huge scale, and retail investors were purchasing GME shares to raise and keep the price high.

What is a short squeeze? A short squeeze can happen when those shorting a stock are forced to repurchase shares at a higher price due to market movements. This repurchasing at higher prices can cause the stock’s price to climb even higher. In the case of GME, the activity of retail investors forced the large firms shorting the stock to repurchase shares at huge losses.

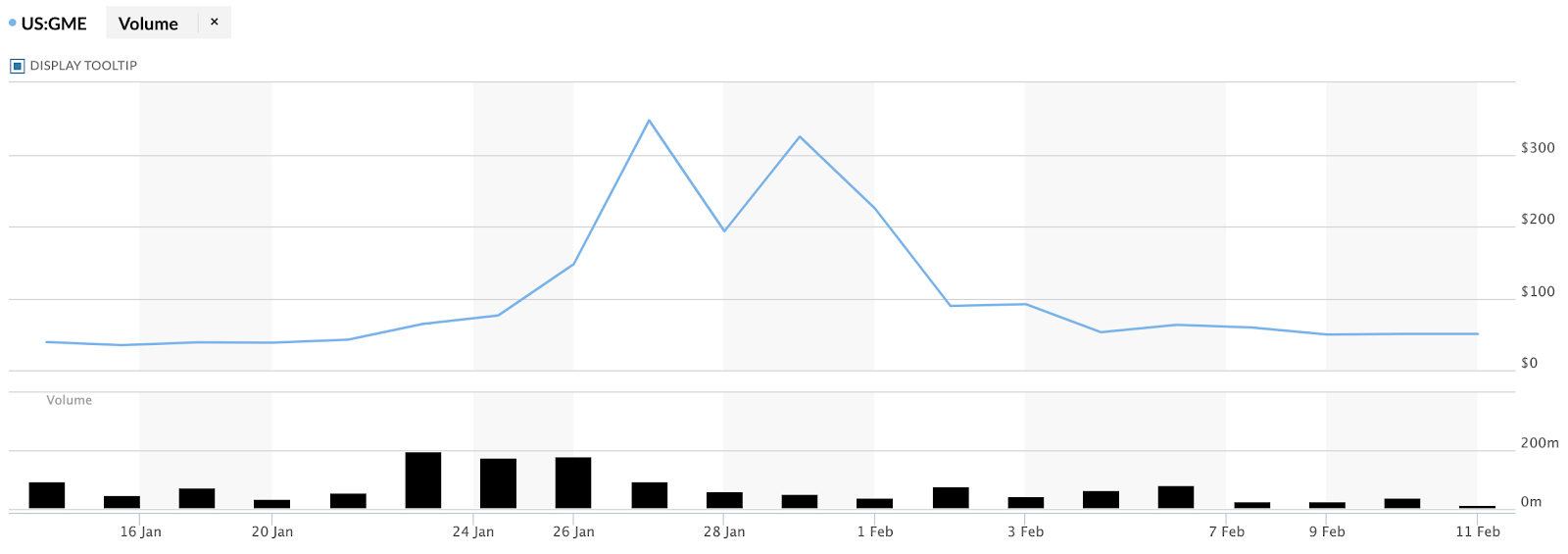

GameStop (GME) Share Price and Volume

Source: MarketWatch

Please check your email for instructions to ensure that the newsletter arrives in your inbox tomorrow.

Was There Foul Play?

As a social media-driven frenzy of buying drove the price of GME ever-higher on the week of January 25, the investment rationale for vigilante small investors, largely associated with the online Reddit forum r/WallStreetBets, was clear: buy and hold. Widespread purchasing of GME would generate returns for those buying in, often at the expense of big investors. These big investors who had shorted the stock were thus forced to buy even more shares — raising the price still higher — or risk facing even greater losses. Then things changed. Retail investors found themselves unable to continue purchasing shares as platforms like Robinhood and Webull limited buys, citing heightened capital requirements due to the unprecedented increase in investments. This seemingly permitted large institutional investors to stop the bleeding and close positions before more damage was done.

Source: Twitter

This turn of events immediately drew ire from those concerned with the potential for foul play, including diametrically opposed political figures like Democratic Representative Alexandria Ocasio-Cortez and Republican Senator Ted Cruz. However, many now accept the capital requirements as a plausible explanation, not the result of some orchestrated plot. Firms have to have a certain amount of capital on hand to cover trades, and Robinhood had to take action to cover the exponential increase in trading volume, at one point needing to raise $3.4 billion to cover new deposits. A forthcoming investigation of what occurred will work to ensure this explanation is valid.

In the meantime, users of such platforms can’t help but point to reasons for collusion. Robinhood directs “more than half of its customer orders” through Citadel Securities, a “financial-services giant.” Part of Citadel came to the rescue of Melvin Capital (a major fund which lost as much as $4.5 billion), and its own fund, Citadel Advisors LLC, was likely trading in GameStop itself, according to the latest available financial reporting from September 2020. Both Robinhood and Citadel have pleaded their innocence, but retail investors see a financial system that recoiled and readjusted when common people were reaping huge profits at the expense of powerful, connected firms. (Further accusations, including that Robinhood forcibly closed some users’ positions in GME and other stocks, appear to be false or misinformed.)

As Wall Street firms were taking big losses, the aggrieved parties decried “market manipulation” by retail investors — effectively suggesting that small-time investors were the ones engaging in foul play. The argument is essentially that these buyers were coordinating in such a way to collectively manipulate the value of specific stocks. Experts have since pointed out that the level of coordination likely does not amount to a level of legal culpability. The discussions of retail investors more likely fall in a gray area somewhere between organized market manipulation and perfectly legal discussions, captured by non-committal sentiments like “we like the stock.” Furthermore, skeptics wonder how hedge funds can take issue with retail investors pursuing a strategy to shift the value of a stock when Wall Street firms regularly employ such strategies themselves.

Another concerning source of potential foul play comes from the ability for anyone to start and fuel trends on social media platforms and forums and then use those public movements to pursue greater profits. Forums like r/WallStreetBets allow experienced and novice investors to intermingle anonymously, and there is very little clarity about who is feeding information and for what reasons. Some have argued that this leaves the door open to manipulation from large investors, many of whom are known to monitor online forums like r/WallStreetBets, or at the very least unscrupulous individuals seeking to take advantage of uninformed investors. In the last few years, several apps have even emerged that allow institutional investors to monitor the trading preferences and discussions of retail investors, helping to identify and take advantage of trends. This makes more sinister manipulation a possibility, though nothing has been verified thus far.

The House Always Wins

Focusing too much on accusations of foul play can distract from the essential details of the day. Who, in the end, made money? Forthcoming investigations will clarify who benefited the most, but evidence suggests that many of those who actually profited are likely to be firms like Senvest, who emerged with an eye-watering $700 million in profit from selling GME, not retail investors. The far more likely scenario is that more small-time investors lost money than made it, all while most big investors were leveraging their range of tools and depth of knowledge to turn a handsome profit.

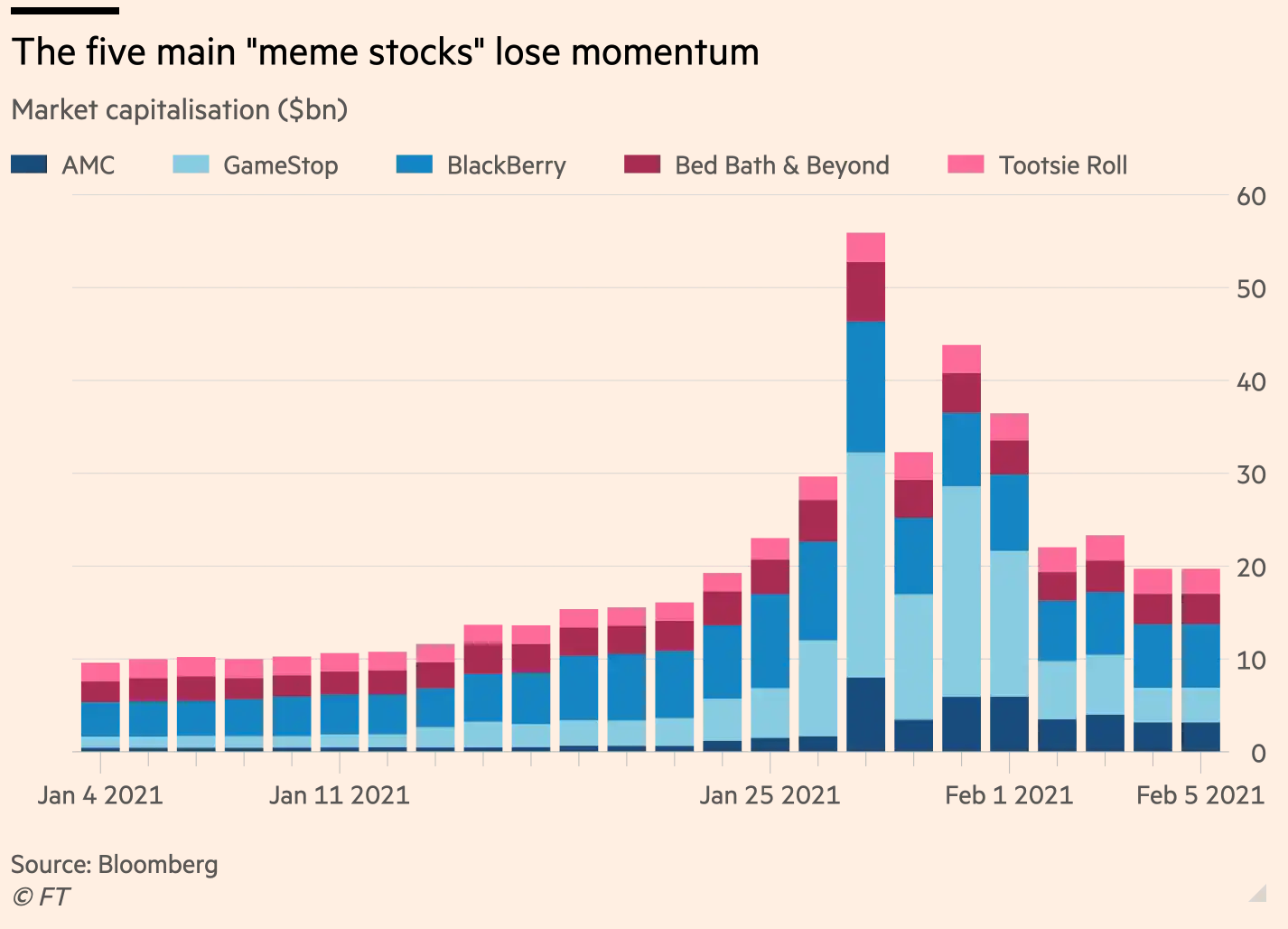

Similar short squeezes occurred with several other stocks, but GME was the most pronounced. Source: Financial Times

To begin with, the gradual growth and explosion of GME was driven not just by r/WallStreetBets followers but institutional investors who began investing in GME months ago. Senvest, for example, owned 5% of the company in October, and according to the Washington Post, the “four largest asset managers in the world together own 39 percent of GameStop shares.” Then, in a flurry of activity over three days, GME shares “changed hands 554 million times — more than 11 times the number of total shares available,” including hundreds of millions of shares being traded at $200 to $300 a share. This volume of trading belies the perceived financial resources and trading rationale (buy and hold) of retail investors working through places like r/WallStreetBets, and rather suggests the hand of informed, large firms buying and selling huge numbers of shares. Simply put, the trading activity suggests that large firms were equally involved in the subsequent boom and bust as small-time investors, undermining the “David vs. Goliath” narrative.

Thinking about the tools and financial acumen of both sides can tell us a lot about who the actual winners and losers are likely to be. On one side, we have well-informed wealthy firms with superior financial acumen, access to and understanding of more sophisticated financial products, and significant trading experience. On the other is a rabble of mostly new investors, enabled by the explosive growth of new trading platforms like Robinhood. These are largely teens and young adults — the average age of users on Robinhood is just 31. A survey cited in MarketWatch found “44% of 1,600 self-directed investors in GameStop and AMC had less than a year of experience trading and another quarter had up to two year’s experience.” The combination of social media-driven hype, questionable crowd-sourced advice, and limited familiarity with sound investment strategies makes these investors far more likely to lose out, exemplified by users who bought in after GME shares were already worth hundreds of dollars. Robinhood is separately under fire for their gamified trading platform, which enables access for new investors but also exposes individuals with no trading experience to financial risk; the company is even facing a wrongful death lawsuit after a 20-year-old user committed suicide in June 2020, fearing he owed over $700,000.

There are endless stories of the small-time investors left holding the bag. These are teens using custodial accounts, working parents taking a risk with some extra cash, and college students with rent to pay. There are certainly cases of individuals who cashed in, but these seem to be far outnumbered by those who dipped their toes into an online trend and paid the price. We know about the huge profits of places like Senvest because they are one of the few firms that has been transparent and outspoken about their success in the scenario, but many other firms have been opaque about their role in the boom and bust. Forthcoming investigations will reveal more, but one retail investor captured the perceived imbalance well in the New York Times: “I realized pretty quick that people like me were up against those billionaires . . . and at the end of the day, those people always find a way to win.”

Please check your email for instructions to ensure that the newsletter arrives in your inbox tomorrow.

Seeking Profit vs. Seeking Payback

Despite losing big, there are many small-time investors who are holding GME as a symbolic gesture to get back at Wall Street, even as its value plummets. There is leftover animosity from the 2008-2009 financial crisis and further anger at how such firms have turned a bumper profit during the pandemic, even as millions go unemployed or face eviction. Whether such firms have a distinct advantage in the markets or not, many in the public seem to think so, and the GameStop boom and bust will only further these sentiments.

For the stalwarts still sticking it to the system, the takeaway is that “Wall Street is absurd and, ultimately, weak. Insiders do whatever they want and get bailed out while normal people . . . lose their houses and jobs.” Americans across the political spectrum seem to agree: “61 percent thought that the government was biased in favor of bankers” and “members of both parties were more likely to call the Redditors heroes than villains.” As long as trust remains low, it will be hard to convince Americans that the stock market works the same for everyone.

Disclosure: The author is an active user of Robinhood but has never owned, nor intends to buy, any of the stocks discussed in this piece.

Note: This Google Sheet lists articles used to inform the findings of this article and indicates how the articles scored according to The Factual’s credibility algorithm. To learn more, read our How It Works page.